October 22, 2015

The Low Cost of Homeownership

TheStreet.com quoted me in Why the Extra Costs of Owning a Home Are Lower Than Consumer Expectations. It reads, in part,

First-time homebuyers are often apprehensive about the extra costs of owning a house, fearful that routine maintenance and repairs will add up quickly, exceeding their original budget.

But their estimates about replacing air filters, mowing the lawn and conducting minor repairs are often much higher than average costs. Consumers have trouble estimating the actual amount and said it would cost $15,070 for home maintenance repairs each year, according to a recent survey by NeighborWorks America, a Washington, D.C-based organization focused on affordable housing.

The actual amount is more likely to be in the range of 1% to 3% of a home’s value or $2,000 to $6,000 nationwide, said Douglas Robinson, a spokesman for NeighborWorks America. Even some current homeowners’ estimates were above the average amount and predicted repairs to cost $12,360. The perception among current renters was even worse with a prediction of $20,503.

“The important thing to remember about buying a home is that there are costs after the purchase that go beyond the monthly mortgage,” he said. “By setting up a savings plan and budget for these costs – items such as landscaping, air conditioning and heating system maintenance – a homeowner will be better equipped to take on the expenses without having to use a credit card or worse, a high-cost emergency loan.”

* * *

Home Emergencies

While they might appear to be rare, homeowners annually should prepare themselves to handle at least one unexpected major emergency such as replacing the boiler or roof in the aftermath of a major storm or flooding in the basement where water needs to be pumped out immediately to protect the foundation, said David Reiss, a law professor at Brooklyn Law School. Establishing an emergency fund would help protect a homeowner when these problems arise so consumers are not forced to turn to more expensive options of debt such as credit cards.

“If a homeowner has an emergency fund, he or she will feel like a genius when it comes time to use it,” he said. “The next step, of course, is to start saving up immediately for the next problem because as most homeowners know – there will be a next problem.”

Some homeowners might find that chronic problems such as the leaky roof are worse than the “acute ones such as the boiler giving out in the winter,” Reiss said.

“This is because we will do whatever it takes to turn the heat back on,” he said. “But we learn to live with the occasional leak and end up feeling like we can ignore it. However, water damage is bad for a house and always gets worse.”

October 22, 2015 | Permalink | No Comments

Thursday’s Advocacy & Think Tank Round-Up

- The Cornerstone Partnership has developed the Inclusionary Calculator, which “allows users to model a real or hypothetical housing development and then add affordable housing requirements in combination with different development incentives.” The Antlantic Citilab has argued that this tool shows that affordable housing is not only feasible but also profitable, almost anywhere. This fact, they argue, makes the decision on whether or not to develop real estate in an inclusionary fashion a moral choice and not an economic one.

- Congratulations to the Empire Community Loan Fund, one of the largest not-for-profit loan funds and Community Development Financial Institution (CDFI), which has been selected for inclusion in the Impact Assets 50 (IA50). The IA 50 is an annual showcase of Impact Investment Fund Managers. The Empire Community Loan Fund issues debt instruments to support affordable housing development, among other things.

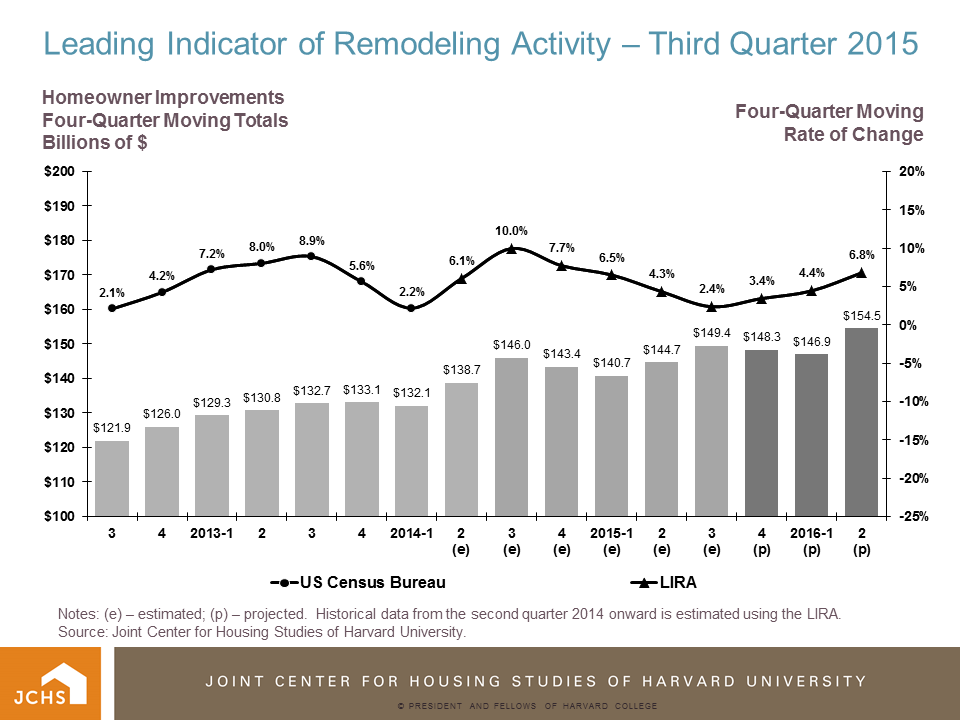

- Harvard’s Joint Center for Housing Studies’ Remodeling Futures Program has released it’s Lead Indicator of Remodeling Activity (LIRA) for the Third Quarter of 2015 in which it predicts annual spending growth for home improvements will accelerate from 2.4% last quarter to 6.8% in the second quarter of 2016. The next LIRA release date is January 21, 2016.

October 22, 2015 | Permalink | No Comments

October 21, 2015

Buy-To-Rent Investing

James Mills, Raven Molloy and Rebecca Zarutskie have posted Large-Scale Buy-to-Rent Investors in the Single-Family Housing Market: The Emergence of a New Asset Class? to SSRN. The abstract reads,

In 2012, several large firms began purchasing single-family homes with the stated intention of creating large portfolios of rental property. We present the first systematic evidence on how this new investor activity differs from that of other investors in the housing market. Many aspects of buy-to-rent investor behavior are consistent with holding property for rent rather than reselling quickly. Additionally, the large size of these investors imparts a few important advantages. In the short run, this investment activity appears to have supported house prices in the areas where it is concentrated. The longer-run impacts remain to be seen.

I had been very skeptical of this asset class when it first appeared, thinking that the housing crisis presented a one-time opportunity for investors to profit from this type of investment. The conventional wisdom had been that it was too hard to manage so many units scattered over so much territory. The authors identify reasons to think that that conventional wisdom is now outdated:

To the extent that technological improvements, economies of scale, and lower financing costs have substantially reduced the operating costs of buy-to-rent investors relative to smaller investors, large portfolios of single-family rental property may become a permanent feature of the real estate market. As such, the events of the past three years may signal the emergence of a new class of real estate asset. A similar transformation occurred in the market for multifamily structures in the 1990s, when large firms began to purchase multifamily property and created portfolios of professionally-managed multifamily units that were traded on public stock exchanges as REITs. (32-33)

Nonetheless, the authors are cautious (rightfully so, as far as I am concerned) in their predictions: “only time will tell whether the recent purchases of large-scale buy-to-rent investors reflect the emergence of a new asset class or whether the business model will fail to be viable over the longer-term.” (33, footnote omitted)

October 21, 2015 | Permalink | No Comments

Wednesday’s Academic Roundup

- Clustered Housing Cycles, Ruben Hernandez-Murillo, Michael Owyang & Margarita Rubio, FRB St. Louis Paper No. FEDLWP2-13-021.

- Crowding Out Effects of Refinancing on New Purchase Mortgages, Steven A. Sharpe & Shane M. Sherlund, FEDS Working Paper No. FEDGFE2015-17.

- The Determinants of Subprime Mortgage Performance Following a Loan Modification, Maximillian D. Schmeiser & Matthew B. Gross, FEDS Working Paper No. FEDGFE2015-06.

- Which Way to Recovery? Housing Market Outcomes and the Neighborhood Stabilization Program, Jenny Schuetz et al., FEDS Working Paper No. FEDGFE2015-04.

- Metropolitan Area Home Prices and the Mortgage Interest Deduction: Estimates and Simulations from Policy Change, Hal Martin & Andrew Hanson, FRB of Cleveland Working Paper No. FEDCWP1516.

- Regional Redistribution Through the U.S. Mortgage Market, Erik Hurst, Benjamin J. Keys, Amit Seru & Joseph Vavra, Kreisman Working Papers Series in Housing Law and Policy No. 25.

- Fewer Vacants, Fewer Crimes? Impacts of Neighborhood Revitalization Policies on Crime, Jonathan S. Spader, Jenny Schuetz & Alvaro Cortes, FEDS Working Paper No. 2015-088.

- Fundamental Drivers of Dependence in REIT Returns, Jamie Alcock & Eva Steiner.

October 21, 2015 | Permalink | No Comments

October 20, 2015

Hypothetically Reforming Fannie and Freddie

S&P issued a report, Fannie, Freddie, and the FHLB System: Plus Ca Change . . . The report opens, “Despite reform talk in the years since the U.S. housing crisis, Standard & Poor’s Ratings Services believes the likelihood of extraordinary government support for key U.S. housing government-related entities (GREs) Fannie Mae, Freddie Mac, and the Federal Home Loan Bank (FHLB) system remains “almost certain” in case of need.” (1) Notwithstanding the fact that S&P expects that this extraordinary support will last well into the next presidential administration, S&P “can envisage three “tail risk” scenarios in which such support could become less likely under certain conditions, but view each of these scenarios as improbable.” (1) The three scenarios, which S&P characterizes as plausible, albeit improbable, are

- An electoral sweep, with favorable macroeconomic conditions and few competing legislative priorities;

- Court judgments, pursuant to shareholder lawsuits, forcing the legislators’ hand; or

- A renewed housing market crisis, with one or more of these GREs viewed as more cause than cure. (4)

In the first scenario, “an election gives one party control of all three legislative actors (the president, House of Representatives, and Senate), precluding the need for bipartisan compromise to enact major reforms to Fannie and Freddie via legislation.” (4)

In the second, Fannie and Freddie shareholders win lawsuits that stem from the “U.S. Treasury’s decision to modify, in 2012, the Preferred Stock Purchase Agreements (PSPAs) governing the terms of its financial support to Fannie and Freddie . . ..” (4)

The final scenario,

is a renewed housing market crisis, on a scale at least similar to that of 2008. Like the other two scenarios, we don’t view this as likely, at least in the coming few years . . . perhaps as a result of the unfortunate confluence of several negative surprises- including, for example, overreaction to Federal Reserve monetary policy normalization, terms-of-trade shocks (geopolitical conflicts that cause a rapid and dramatic spike in energy costs, perhaps), fresh financial sector problems that suddenly tighten the sector’s funding costs, and an abnormally long spell of bad weather. (5)

This seems like a pretty reasonable analysis of the likelihood of reform for Fannie and Freddie. But that should not stop us from bemoaning Congressional inaction on this topic. Obviously, Congress is too ideologically driven to bridge the gap between the left and right, but the likelihood that we are building toward some new kind of crisis increases with time. I can’t improve on S&P’s analysis in this report, but I’m sure unhappy about what it means for the long-term health of our housing finance system.

”

October 20, 2015 | Permalink | No Comments

Tuesday’s Regulatory & Legislative Update

- The Consumer Financial Protection Bureau (CFPB) has finalized a Rule to expand reporting requirements imposed upon financial institutions under the Home Mortgage Disclosure Act (HMDA). Dodd-Frank included a mandate directing the CFPB to collect metrics to allow, among other things, a better understanding of the mortgage market, quicker identification of trends, and spotting of discriminatory patterns and practices. The CFPB also hopes to use the data to avoid some of the mistakes in the mortgage market which led to the Financial Crisis. The CFPB also has a site containing resources to help financial institutions comply.

- CFPB has released the prepared remarks of Director Richard Corday, which he delivered before the Mortgage Bankers Association’s Annual Convention. In discussing the new agency’s work since Dodd-Frank, Corday asserted that the CFPB has worked hard to create a “set of rules that protect prospective homebuyers in a manner that never existed in the past, while supporting responsible lenders against those who led a race to the bottom in underwriting standards. We now have a system in place that consumers can trust in a way they could not trust in the marketplace a decade ago.”

- The Terwilliger Foundation hosted a Housing Summit in New Hampshire where Presidential Hopefuls, including, among others: Martin O’Malley, Chris Christie, George Pataki), Mike Huckabee, and Rand Paul. The Enterprise Community Partners Blog has a great piece which describes the affordable housing policy proposals of the various candidates.

October 20, 2015 | Permalink | No Comments

October 19, 2015

Kickbacks in Residential Transactions

The Consumer Financial Protection Bureau has issued Compliance Bulletin 2015-05, RESPA Compliance and Marketing Servicing Agreements. The Bulletin opens,

The Consumer Financial Protection Bureau (CFPB or the Bureau) issues this compliance bulletin to remind participants in the mortgage industry of the prohibition on kickbacks and referral fees under the Real Estate Settlement Procedures Act (RESPA) (12 U.S.C. 2601, et seq.) and describe the substantial risks posed by entering into marketing services agreements (MSAs). The Bureau has received numerous inquiries and whistleblower tips from industry participants describing the harm that can stem from the use of MSAs, but has not received similar input suggesting the use of those agreements benefits either consumers or industry. Based on the Bureau’s investigative efforts, it appears that many MSAs are designed to evade RESPA’s prohibition on the payment and acceptance of kickbacks and referral fees. This bulletin provides an overview of RESPA’s prohibitions against kickbacks and unearned fees and general information on MSAs, describes examples of market behavior gleaned from CFPB’s enforcement experience in this area, and describes the legal and compliance risks we have observed from such arrangements. (1, footnote omitted)

RESPA had been enacted to curb industry abuses in residential closings. Segments of the industry have been very creative in developing new strategies to avoid RESPA liability, with MSAs a relatively new twist. MSAs are often “framed as payments for advertising or promotional services” but in some cases the providers “fail to provide some or all of the services required under their agreements.” (2,3)

This Bulletin is a shot across the bow of industry participants that are using MSAs, reminding them of the significant penalties that can result from RESPA violations. It seems to me that the Bureau is right to warn industry participants to “consider carefully RESPA’s requirements and restrictions and the adverse consequences that can follow from non-compliance.” (4)

October 19, 2015 | Permalink | No Comments

{kind=link}