- Capital New York reports another study which finds that non-whites are at a disadvantage when it comes to securing a home loan, this is more pronounced in the conventional loan market (less so for FHA loans). Includes an interactive chart which breaks down the stats by borough.

- Harvard’s Joint Center for Housing Studies’ Annual State of the Nation’s Housing 2015 reveals historic lows in homeownership rates, and a corresponding “rental boom,” a shortage in supply for single family dwellings, and an increasingly severe rental affordability problem.

- National Association of Realtors’ release of Existing Home Sales statistics for May reveal a strong rebound over April, in fact sales are strongest they have been in 6 years, with first time homebuyers making up the biggest portion of buyers.

- NYU Furman Center’s new working paper – Utility Allowances in Federally Subsidized Multifamily Housing – advocates four policy changes which would help HUD increase energy efficiency in the properties it subsidizes. These include, 1. Incentivizing owners to switch to individually metered units; 2. Incentivizing owners to make energy saving upgrades; 3. Provision of utility allowances that are affordable but make recipients bear the cost of consumption; 4. Provide information about relative utility costs to increase tenant purchasing power.

Tag Archives: National Association of Realtors

Thursday’s Advocacy & Think Tank Round-Up

- National Association of Realtors reports April Pending home sales, up 1.3% – the strongest in 9 years.

- A joint study by the NYU Furman Center and Capital One Renting in America’s Largest Cities: National Affordable Rental Housing Landscape reveals a trend in all 11 of the largest metro areas in the U.S., which the study focused on, of rent increases outpacing inflation, tending to not keep up with the increase in number of renters and an increase in severely rent burdened low income renters.

- Zillow’s recent research concludes that the rent affordability crisis leads to lower homeownership rates because renters cannot afford to save for a downpayment in high rent metros like Los Angeles.

Thursday’s Advocacy & Think Tank Round-Up

- City lab’s analyzes why Billionaires Don’t Pay Taxes in New York, concludes that recent housing boom has been in the “ultralux” market and that the owners pay a fraction of their share due to a tax code that shifts the burden from owners to renters and from the wealthy to the poor.

- The Center on Budget and Policy Priorities released an analysis of federal housing subsidy programs and their effectiveness

- Corelogic’s National Foreclosure Report for March 2015 finds that while delinquency rates are down to 3.9% the percentage of mortgagees struggling to make their payments is still above pre-recession levels.

- National Association of Realtors released data showing decreased homeownership rates across regional metro areas of the U.S., analysis of this data lead to the conclusion that continued decline in homeownership means the gains are going to fewer people and likely leading to worsening inequality in the U.S.

- The Roosevelt Institute’s Rewriting the Rules of the American Economy: An Agenda for Growth and Prosperity by Joseph Stieglitz, seeks to completely revamp the rules and regulations that shape our economy, corporate behavior and the financial sector – with a view toward creating shared prosperity. Proposals related to real estate finance include, providing §11 bankruptcy protection for homeowners and creating a public option for the supply of mortgages.

- The Urban Institute released Welding a Heavy Enforcement Hammer has Unintended Consequences for FHA Mortgage Market concludes that the significant, easily triggered liability of both the False Claims Act and the Financial Institutions Reform, Recovery, and Enforcement Act have had a chilling effect, causing some lenders to do less origination to reduce their litigation risk.

Thursday’s Advocacy & Think Tank Round-Up

- Enterprise Community Partners and the National Low Income Housing Coalition and 45 other affordable housing advocates signed a letter to the appropriations committees of the house and senate urging them to pride at least $1.2 billion for the HOME Investment Partnerships Program (HOME). a block grant that provides states and localities critical resources to help them respond to affordable housing challenges.

- A recent study by the National Association of Realtors finds that formerly distressed homeowners with restored credit are re-entering the housing market, nearly a million of these former owners have likely already purchased a home again, and an additional 1.5 million are likely to become eligible and purchase over the next five years, representing an additional source of buyer demand for the housing market.

- National Association of Realtors also released it’s March Realtor Confidence Index which finds gains in home sales and prices but noted concern over lender delays and tight inventory, especially for affordable units.

Thursday’s Advocacy & Think Tank Round-Up

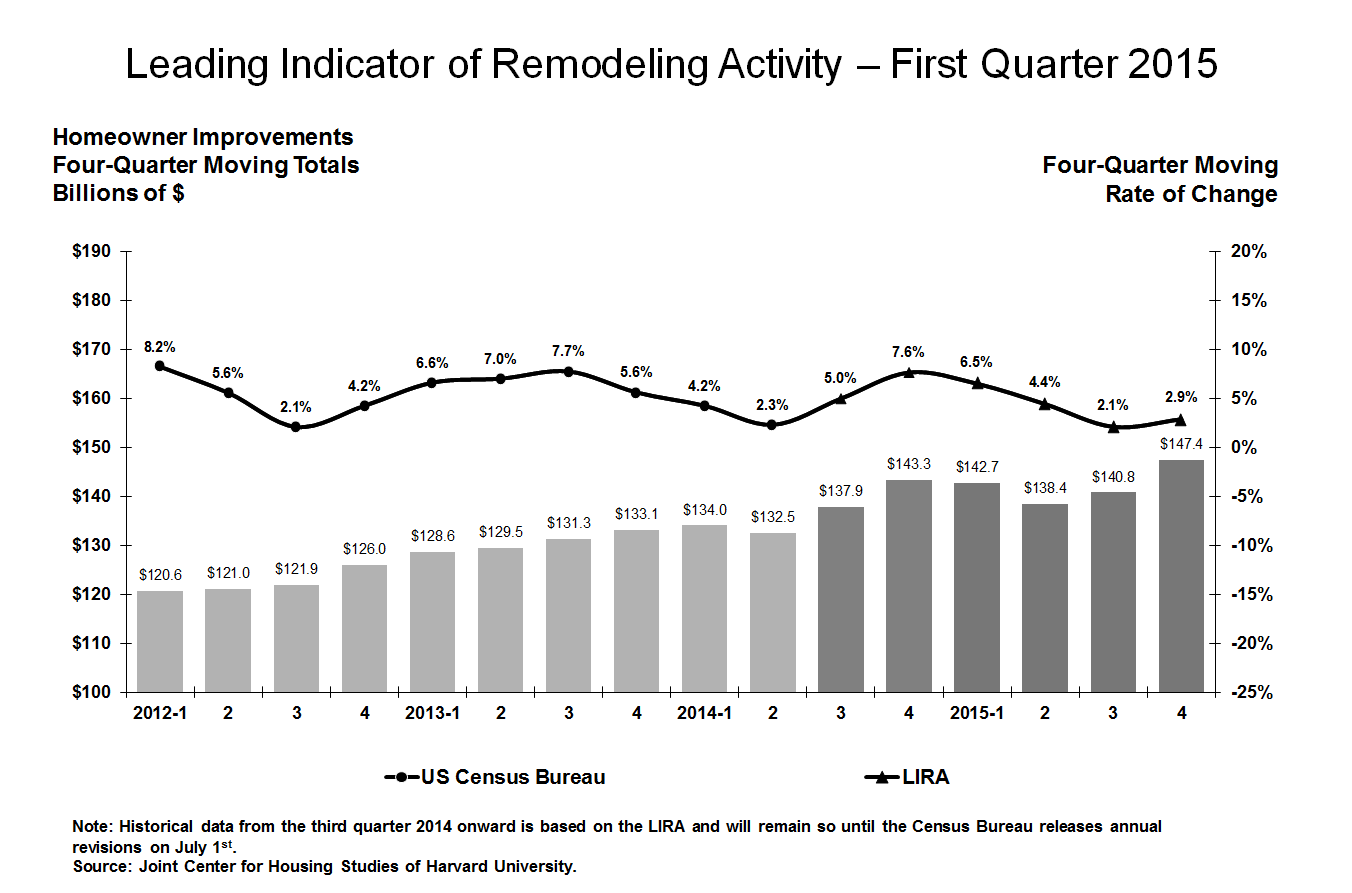

- Harvard’s Joint Center for Houses Studies released its Leading Indicator of Remodeling Activity (LIRA) which predicts a deceleration in remodeling activity due to sluggish home sales, the LIRA also projects annual spending for home improvements will increase a more modest 2.9% in 2015.

- National Association of Realtors’ testimony before the United States Senate Committee on Banking, Housing and Urban Affairs, Hearing titled Regulatory Burdens to Obtaining Mortgage Credit, argues that unnecessary burdens prevent qualified buyers from obtaining mortgages in today’s market.

Thursday’s Advocacy & Think Tank Round-up

- Brookings Institution Spring 2015 Brookings Panel on Economic Activity Research Paper: Risk Management for Monetary Policy Near the Zero Lower Bound Concludes that It Is Better if Interest Rates Stay Low Rather than be Raised Too Soon.

- Center on Budget and Policy Priorities Report: Highlights How President Obama’s Budget Will Restore 67,000 Housing Vouchers lost During the 2013 Sequestration

- Federal Reserve Board’s Division of Research & Statistics and Monetary Affairs, Report: Crowding out Effects of Refinancing on New Purchase Mortgages, Concludes that High Credit Risk Borrowers Get Approved for Mortgage Loans Nire often When Interest Rates are High.

- The Federal Reserve Board’s Consumer and Community Development Research Team evaluated the success of Neighborhood Stabilization Program in, Have Distressed Neighborhoods Recovered?

- New Climate Economy Report: Provides Comprehensive Estimates of the Costs of Sprawl and Potential Benefits of Smart Growth, Describes Planning and Market Distortions that Foster Sprawl, and Smart Growth policies that can help correct these distortions.

- National Association of Realtors Letter to Senators Delany (D-MD) and Others Thanking them for Re-Introducing the Partnership to Strengthen Home Ownership Act, which would Reform the Housing Finance System

Thursday’s Advocacy & Think Tank Round-up

- ACLU: “Here We Go Again: Communities of Color, The Foreclosure Crisis, and Loan Servicing Failures”

- Federal Housing Finance Agency – HPI Calculator – projects what a given house purchased at a point in time would be worth today if it appreciated at the average appreciation rate of all homes in the area.

- Federal Reserve Bank of New York Interactive Home Price Index – Maps changes in home prices each month compared with prices one year earlier, by county, based on CoreLogic overall house price indexes.

- Joint Center for Housing Studies Harvard University: “Racialized Recovery: Post-Forclosure Pathways in Distressed Neighborhoods in Boston”

- National Association of Realtors – Realtors Confidence Index Reflects on Positive Trends in Home Sales for January

- Urban Institute’s Housing Finance Policy Brief “The U.S. Treasury’s Credit Rating Agency Exercise: First Steps Out of the Private Label Securities Desert”

{kind=link}